Mark-Et Minute 2/25/2025

Year to Date Market Indices as of February 25th, 2025

• Dow 43,584 (2.4%)

• S&P 5,957 (1.29%)

• NASDAQ 19,078 (-0.12%)

• OIL $68.79 (-4.26%)

• Barclay Bond Aggregate (1.9%)

• Gold $2,905 (10.52%)

Addressing Investor Questions on Tariffs and Inflation

An examination of the potential impact of the proposed levies on U.S. trading partners.

With the Trump administration’s plans to implement a broad range of tariffs on U.S. trading partners in coming weeks, we have received queries from investors on how these levies may affect the pace of future U.S. inflation. Here, we examine five of the most important questions.

1. Do tariffs by themselves lead to a pickup in overall inflation?

Historically, tariffs are not inflationary in that they do not set off a permanently higher rate of price increases. Their implementation typically results in a level upward adjustment of the price of tariffed goods by some amount; what sustains that rate of increase is broader conditions in the economy. Tariffs certainly have a cost. They have the same effect as a price increase stemming from any other cause, in that people will pay more for the goods they are buying. But as long as tariffs are not increased, they have a one-time effect and so do not permanently accelerate the rate at which prices are increasing. Typically, they drop off after some period, at which point the inflationary effect goes away.

Bottom line, the tariffs do increase prices for consumers, but they don’t by themselves usher in higher inflation.

2. What about the impact on inflation expectations?

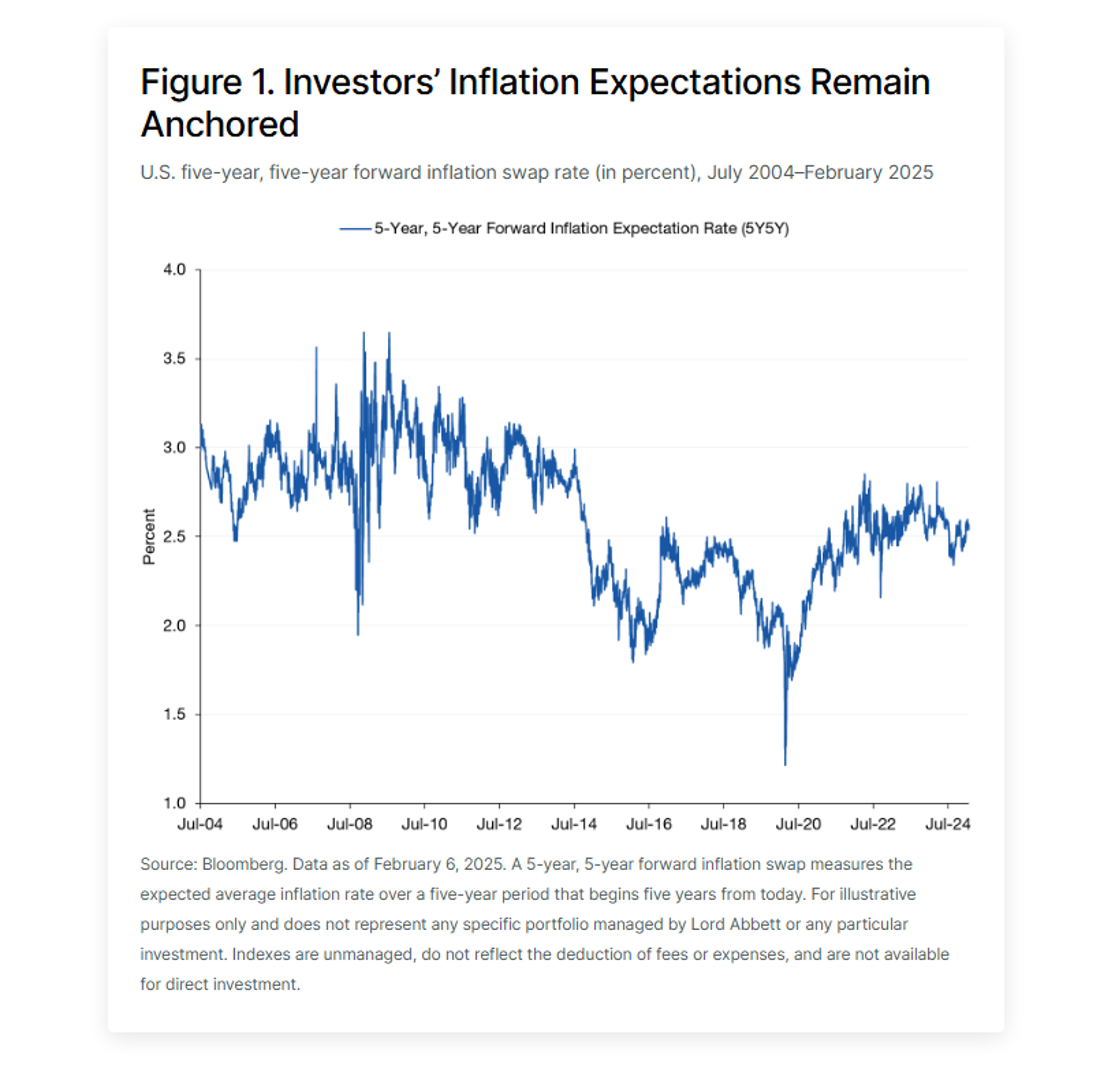

This is where things get a little trickier. The recent COVID-driven price shock did cause inflation expectations to rise among consumers, businesses, and investors, but since the inflation data began to moderate in mid-2022, those expectations have been reasonably well anchored, remaining in a narrow range for the past several months (see Figure 1).

But when you look back at historical U.S. inflation episodes like the double-digit increases seen in the 1970s, they started as a tight economy received an initial shock (e.g., a spike in oil prices), followed by a series of policy decisions (wage and price controls, a reluctance to hike interest rates in the face of spiraling prices) that exacerbated the situation.

Fast forward to early 2025. The recent tariff announcements have come at a time when consumers and businesses have been sensitized to price increases after the long stretch of low inflation that preceded the COVID episode (in the 10 years before the onset of the pandemic in early 2020, monthly readings of the year-over-year headline U.S. consumer price index [CPI] ranged from -0.1% to 3.9%). Nonetheless, as Figure 1 shows, the big inflation shock of 2021-22 did not results in expectations becoming de-anchored.

However, the waters have been muddied by a much higher-than-expected 0.5% increase in the headline CPI for January 2025, as reported by the U.S. Bureau of Labor Statistics on February 12. A fresh uptick in prices, coming amid the expected imposition of double-digit tariffs across a range of nations and product categories, may give businesses a greater propensity to raise prices if they expect inflation to trend higher in coming months. Another jump in prices, coming as the memories of the 2021-22 episode are still fresh, may translate into a larger increase in inflation expectations than would be expected based on the last one in isolation. In other words, expectations for future prices risk getting destabilized by repeated shocks after many years of relative calm. Of course, the situation remains fluid, and the amounts of, and timetables for, proposed tariffs are subject to change.

3. How long does it take for tariffs to influence prices?

The most recent evidence (based on observations in 2019 after the implementation of tariffs in the first Trump administration) shows that tariffs are fully passed through into selling prices and/or margins of importing companies, either to consumers in the form of higher selling prices or coming out of importers’ margins. The full effect is not felt immediately; there is typically a 12 to 24-month lag.

One other thing to note is that while the stated intent of tariffs is to create an economic penalty on overseas goods producers, the brunt of the levies is borne by (1) U.S.-based firms who might absorb it into lower margins, and (2) by consumers, in the form of higher selling prices for goods.

4. Any impact on prices of domestically produced goods?

Tariffs directly affect the price of imported goods, but there also is solid evidence that there is an umbrella effect, in which domestic competitors for those imported goods also raise their prices.1 That would seem to be a rational response, especially if those domestic producers are capacity constrained in the short run. Producers of substitute goods (from a similar but not directly comparable category) also tend to raise prices.

There is also another potential effect on so-called complementary goods—those typically sold with the tariffed items. A 2020 study provides an example: In the last round of tariffs, duties were assessed on Chinese-made washing machines. The domestic selling price of washers increased directly (around 8%) as a result. Clothes dryers were not tariffed, but since washers and dryers are complementary goods (people tend to buy both at the same time), the price of dryers also increased by 8%, even though they were not subject to tariffs.

5. Would a stronger U.S. dollar offset the effects of tariffs?

Imported goods might be made more expensive by being tariffed, but that impact could be offset by movements in the currency, and recent studies suggest that something between 20% to 50% of the effect of the tariff is offset by a stronger dollar, as strength in the U.S. currency makes imported goods cheaper than they otherwise would be.3

However, a firmer dollar has a competitive penalty associated with it for U.S. exporters, because it makes U.S.-manufactured goods more expensive. So, the offset from a stronger currency is not an unambiguous benefit.

Market Moving News

Shopping slowdown

U.S. consumers trimmed their spending more than expected after the holiday shopping season. In January, retail sales fell 0.9% on a seasonally adjusted basis compared with the previous month. The result was well below most economists’ expectations and marked the biggest monthly decline in a year.

Sticky inflation

Wednesday’s Consumer Price Index report extended a recent trend of slightly hotter-than-expected inflation. Core inflation, excluding volatile energy and food prices, rose at an annual rate of 3.3% in January. That result was above economists’ consensus forecast and slightly above the previous month’s annual figure.

Fed’s rate wait

U.S. Federal Reserve Chair Jerome Powell said in congressional testimony that Fed policymakers need to see more progress in curbing inflation before considering further interest-rate cuts. Powell declined to specify the inflation rate that might trigger the Fed to approve a further cut in its benchmark rate, which has remained in a range of 4.25% to 4.50% since the last cut in December.

https://www.marketwatch.com/ (Market Indices)

https://www.jhinvestments.com/weekly-market-recap#market-moving-news

https://www.lordabbett.com/en-us/financial-advisor/insights/markets-and-economy/2025/addressing-investor-questions-on-tariffs-and-inflation.html

The views presented are not intended to be relied on as a forecast, research or investment advice and are the opinions of the sources cited and are subject to change based on subsequent developments. They are not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investments.